1.7: Economic Systems

- Page ID

- 1627

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Economic Systems

Every society has an economy or economic system that helps it provide necessities for the people. The economy or economic system is an organized way of providing for the wants and needs of their people. Every economy has to deal with the concept of scarcity and must answer the questions “what to produce?”, “how to produce?” and “for whom to produce?”

Universal Generalizations

- Capitalism, socialism, and communism are the three major economic systems.

- All economic systems have advantages and disadvantages.

Guiding Questions

- What are the advantages and disadvantages of capitalism?

- What is the difference between socialism and communism?

- How is communism both an economic and a political system?

Think about what a complex system a modern economy is. It includes all production of goods and services, all buying and selling, and all employment. The economic life of every individual is interrelated, at least to a small extent, with the economic lives of thousands or even millions of other individuals. Who organizes and coordinates this system? Who ensures that the number of televisions a society provides is the same as the amount it needs and wants? Who ensures that the right number of employees work in the electronics industry? Who insures that televisions are produced in the best way possible? How does it all get done?

Traditional Economy

There are at least three ways societies have found to organize an economy. The first is the traditional economy, which is the oldest economic system and can be found in parts of Asia, Africa, and South America. Traditional economies organize their economic affairs the way they have always done (i.e., tradition). Occupations stay in the family. Most families are farmers who grow the crops they have always grown using traditional methods. What you produce is what you get to consume. Because things are driven by tradition, there is little economic progress or development.

In a society with a traditional economy, the allocation of resources stems from ritual, habit, or custom. This type of economic system also guides the society since the roles regarding people's jobs are defined by the custom of elders and ancestors. The expectation is that the members of the community carry on the skills of the previous generation Therefore, the custom is for children to continue to practice the same role as the parents. Girls learn their role from their mothers and other female adults, while boys learn their economic and social role from their fathers or other male adults. If you are a son of a farmer, you too will be a farmer. This type of social conformity makes it possible for the group to survive from one generation to the next.

A Command Economy

Command economies are very different. In a command economy, economic effort is devoted to goals passed down from a ruler or ruling class. Ancient Egypt was a good example: a large part of economic life was devoted to building pyramids, for the pharaohs [Figure 1]. Medieval manor life is another example: the lord provided the land for growing crops and protection in the event of war. In return, vassals provided labor and soldiers to do the lord’s bidding. In the last century, communism emphasized command economies.

[Figure 1] - Ancient Egypt was an example of a command economy. (Credit: Jay Bergesen/Flickr Creative Commons)

In a command economy, the government decides which goods and services will be produced and what prices will be charged for them. The government decides what methods of production will be used and how much workers will be paid. Many necessities like healthcare and education are provided for free and may be considered a strength of the economy. However, the disadvantages of the system, such as not catering to consumers, little incentive to work harder or better, the large bureaucracy, lack of flexibility, and no rewards for individual initiative or unique ideas, creates a stagnant marketplace. Currently, Cuba and North Korea have command economies.

A Market Economy

A market is an institution that brings together buyers and sellers of goods or services, who may be either individuals or businesses. Although command economies have a very centralized structure for economic decisions, market economies have a very decentralized structure. In a market economy, decision-making is decentralized. Market economies are based on private enterprise: the means of production (resources and businesses) are owned and operated by private individuals or groups of private individuals.

[Figure 2] Nothing says “market” more than The New York Stock Exchange. (Credit: Erik Drost/Flickr Creative Commons)

The New York Stock Exchange, shown in [Figure 2], is a prime example of a market in which buyers and sellers are brought together. Businesses supply goods and services based on demand. (In a command economy, by contrast, resources and businesses are owned by the government.) The goods and services supplied depend on what is demanded. A person’s income is based on his or her ability to convert resources (especially labor) into something that society values. The more society values the person’s output, the higher that person's income (think Lady Gaga or LeBron James). In this scenario, economic decisions are determined by market forces, not governments.

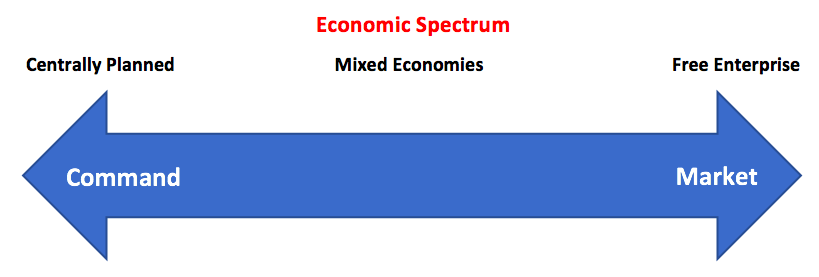

Most economies in the real world are mixed; they combine elements of command and market (and even traditional) systems. The U.S. economy is positioned toward the market-oriented end of the spectrum. Many countries in Europe and Latin America, while primarily market-oriented, have a greater degree of government involvement in economic decisions than the U.S. economy does. China and Russia, while they are closer to having a market-oriented system now than several decades ago, remain closer to the command economy end of the spectrum. A rich resource of information about countries and their economies can be found on the Heritage Foundation’s website.

The economic spectrum demonstrates the range of possible economic systems used by societies.

Who is in control of economic decisions? Are people free to do what they want and to work where they want? Are businesses free to produce when they want and what they choose, and to hire and fire as they wish? Are banks free to choose who will receive loans? Or does the government control these kinds of choices?

| Traditional | Command | Market | |

| Advantages |

|

|

|

| Disadvantages |

|

|

|

Each year, researchers at the Heritage Foundation and the Wall Street Journal look at 50 different categories of economic freedom for countries around the world. They give each nation a score based on the extent of economic freedom in each category.

The 2013 Heritage Foundation’s Index of Economic Freedom report ranked 177 countries around the world: some examples of the most free and the least free countries are listed in Table 1. Several countries were not ranked because of extreme instability that made judgments about economic freedom impossible. These countries include Afghanistan, Iraq, Syria, and Somalia.

|

Most Economic Freedom |

Least Economic Freedom |

|

1. Hong Kong |

168. Iran |

| 2. Singapore | 169. Turkmenistan |

| 3. Australia | 170. Equatorial Guinea |

| 4. New Zealand | 171. Democratic Republic of Congo |

| 5. Switzerland | 172. Burma |

| 6. Canada | 173. Eritrea |

| 7. Chile | 174. Venezuela |

| 8. Mauritius | 175. Zimbabwe |

| 9. Denmark | 176. Cuba |

| 10. United States | 177. North Korea |

The assigned rankings are inevitably based on estimates, yet even these rough measures can be useful for discerning trends. In 2013, 91 of the 177 included countries shifted toward greater economic freedom, although 78 of the countries shifted toward less economic freedom. In recent decades, the overall trend has been a higher level of economic freedom around the world.

Video: Economic Systems and Macroeconomics

As previously addressed, market systems and command systems in their pure form are on the extremes of the economic spectrum, and in reality each fails to exist entirely in isolation of the other. More accurately, all nations operate under a "mixed economic system" that emulates certain characteristics of each type of economy to varying degrees.

In a pure command economy, rather than businesses and individuals, because government owns the means of production, they determine what to produce, how to produce it, and who gets it once it has been produced. This is an incredibly difficult and complicated process that limits the free will of the people living within its rules. Central planners (government officials) make decisions based on what they believe is best for the population.

In a pure market economy, there is no government intervention. The prices of goods and services are entirely set by the demand and supply of what is available. This is known as the "price system." Thus there is competition amongst buyers and sellers in a market economy. Buyers are trying to outbid other buyers by offering a higher price. Whereas sellers are competing with other sellers by offering lower prices and/or higher quality goods and services.

Regardless of what type of economic system a nation has, there are three questions that each must answer. How the nation answers these questions determines whether it is a more market or command-leaning economic system. These three questions were covered in an earlier section, but to review:

- What is to be produced?

- Given the resources a country has at its disposal, it could make any great number of things. Who decides how an economy is going to utilize those productive resources to produce things determines whether the economy is more command or market.

- How are those goods and services going to be produced?

- In a market economy, businesses (firms) decide how goods and services are going to be produced. They hire labor as they see fit and pay accordingly.

- In a command economy, the government plays a large part in directing certain people to be responsible for producing goods and providing services, and is likely to set a wage that is very similar to other wages for different work.

- For whom are goods and services going to be produced?

- This is a question that focuses on who is going to receive the goods and services that are being produced. In a market economy, this would be largely determined by the consumers who can afford to purchase the goods and services they demand.

- In a command economy the government would decide who receives which goods and services.

Whether a nation's economy is labeled as a market or command economy is determined by who makes these decisions. In a market economy, most of the decisions are made privately by consumers and firms about what to produce, how to produce it, and who receives it. In a command economy, all decisions are carried out by government officials. As stated earlier, most economies are mixed, where economic decisions are sometimes made by individuals and private firms, while others are put in place by government officials.

Economic Goals

Countries go about attempting to create stability for their economy by fulfilling various economic goals. While all societies work toward each of the goals listed below to some extent, societal values are the differentiating factors that determine to what degree each goal is pursued. Economic efficiency, freedom, security, equity, and growth are all values that determine to what extent the economic players are involved, and since countries do not always agree on what the most important economic goals are, some goals are more valued than others. Below is a brief explanation of each economic goal. As you read through the numbered list, contemplate which goals would be more important to a market economy and which would be more important for a country with a command economy.

- Economic Efficiency

Efficiency is focused on making sure that the available resources are used to the fullest extent to produce the most wanted goods and services demanded by the people. When an economy is efficient, it is organized and maximizes production.

When an economy isn't focused on efficiency, it may be more wasteful in the utilization of its resources and less responsive to the demands of the people.

- Economic Equity

Equity refers to promoting fairness. To ensure equity, a government may redistribute wealth among its citizens. This means the government may tax wealthier people at a higher percentage than the rest of the population and then provide social welfare programs to the poorer populations. Low income families would receive assistance in terms of food stamps, cheaper housing, medical care, or qualifying education grants.

When an economy isn't focused on equity, it would do little to ensure that the poor or lower-income population have access to the goods and services readily available to those who can easily afford them.

- Economic Freedom

Freedom in an economic sense means that one is able to make decisions about what goods and services to buy or sell, and how to live without any restrictions by a governing body. Obviously complete freedom would be problematic because potentially harmful trade would be legal, putting the safety of citizens at risk. For this reason, no economy can be entirely free.

Economies become less free when they tax more, restrict certain forms of trade, and control the means of production.

- Economic Growth

Growth in an economy is measured by a continual increase in the production of goods and services. As a result of economic growth, the standard of living improves, meaning people are making more money, the population is able to grow, and education levels rise.

Countries that lack economic growth tend to be inefficient with their resources and lack a feeling of optimism about the future. Without adequate economic growth these countries face problems with their security as well.

- Economic Security

A country that provides a high level of economic security alleviates the fear individuals might feel when it comes to the occurrence of economic risks over which an individual has very little control. For example, if a country were to suffer a natural disaster, or go to war, experience massive unemployment, individuals would want to know that they are going to have their needs met so they can provide for themselves and their families.

Countries that lack economic security usually have no safety net available for those who are affected by forces outside of their control. These systems lack government programs like food stamps, unemployment benefits, public housing, and Social Security. Without these programs in place, those who are affected by such events have little chance of surviving on their own financially.

- Economic Stability

Stability comes when three major measures of economic well-being are met:

- The economy is consistently growing.

- Unemployment rates are relatively low and consistent.

- Prices are maintained at the same level.

Countries that lack economic stability will experience harmful swings that discourage people from spending money in their economy which stalls growth and improvement.

In conclusion, all economic systems are designed to manage the production, consumption, and distribution of goods and services, they simply have varying degrees of control along the economic spectrum.

Use the resources below to further investigate these concepts:

Index of Economic Freedom

Explore the interactive heat map of economic freedom at the website below. This map demonstrates the relative economic freedom of different countries throughout the world. Which are more likely to be market economies? Which are more likely to be command economies?

Communism or Socialism?

For clarification on the difference between communism and socialism, read the following article by David Floyd:

Video: Why is Communist China Doing So Well?

Watch this video by economics teacher Jacob Clifford to learn how a the communist country of China has been using the free market to grow its economy.

Answer the self check questions below to monitor your understanding of the concepts in this section.

Self Check Questions

- What are at least three ways societies have found to organize economy?

- Describe the differences between traditional, command and market economies. Give advantages and disadvantages for each.

- List the six economic goals and give a brief description for each.

- What are some differences between communism and socialism?

- Why might a country move from one economic system to another?