4.11: The Federal Reserve System

- Page ID

- 1707

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)The Federal Reserve System

The Federal Reserve System was established in 1913 as the nation’s central bank. It is owned by private member banks, not by the government. It regulates financial institutions, conducts monetary policy, provides services to the government, maintains the payment system, and enforces consumer protection laws. In addition, it supervises member banks, bank holding companies, and international operations of commercial banks, it maintains the country’s currency, clears checks, and oversees truth-in-lending laws.

Universal Generalizations

- The Federal Reserve works to strengthen and stabilize the nation’s monetary system.

- The Federal Open Market Committee makes decisions about the growth of the money supply.

- The Fed has a broad range of responsibilities, regulating both banks and laws to protect consumers.

Guiding Questions

- What is a difference between National banks and State Banks in regard to the Fed?

- What is the main role of the Board of Governors for the Federal Reserve System?

Marriner S. Eccles Federal Reserve Headquarters, Washington D.C.

Some of the most influential decisions regarding monetary policy in the United States are made behind these doors. (Credit: modification of work by “squirrel83”/Flickr Creative Commons)

The Federal Reserve Banking System and Central Banks

In making decisions about the money supply, a central bank decides whether to raise or lower interest rates and, in this way, to influence macroeconomic policy whose goal is low unemployment and low inflation. The central bank is also responsible for regulating all or part of the nation’s banking system to protect bank depositors and ensure the health of the bank’s balance sheet.

The organization responsible for conducting monetary policy and ensuring that a nation’s financial system operates smoothly is called the central bank. Most nations have central banks or currency boards. Some prominent central banks around the world include the European Central Bank, the Bank of Japan, and the Bank of England. In the United States, the central bank is called the Federal Reserve—often abbreviated as just “the Fed.” This section explains the organization of the U.S. Federal Reserve and identifies the major responsibilities of a central bank.

Structure/Organization of the Federal Reserve

Unlike most central banks, the Federal Reserve is semi-decentralized. It mixes government appointees with representation from private-sector banks. At the national level, it is run by a Board of Governors, consisting of seven members appointed by the President of the United States and confirmed by the Senate. Appointments are for 14-year terms and they are arranged so that one term expires January 31 of every even-numbered year. The purpose of the long and staggered terms is to insulate the Board of Governors as much as possible from political pressure so that policy decisions can be made based only on their economic merits. Additionally, except when filling an unfinished term, each member only serves one term, further insulating decision-making from politics. Policy decisions of the Fed do not require congressional approval, and the President cannot ask for the resignation of a Federal Reserve Governor as the President can with cabinet positions.

One member of the Board of Governors is designated as the Chair. For example, from 1987 until early 2006, the Chair was Alan Greenspan. From 2006 until 2014, Ben Bernanke held the post. The current Chair, Jerome Powell, was sworn-in in February 2018. The Fed Chair is first among equals on the Board of Governors. While he or she has only one vote, the Chair controls the agenda and is the public voice of the Fed, so he or she has more power and influence than one might expect.

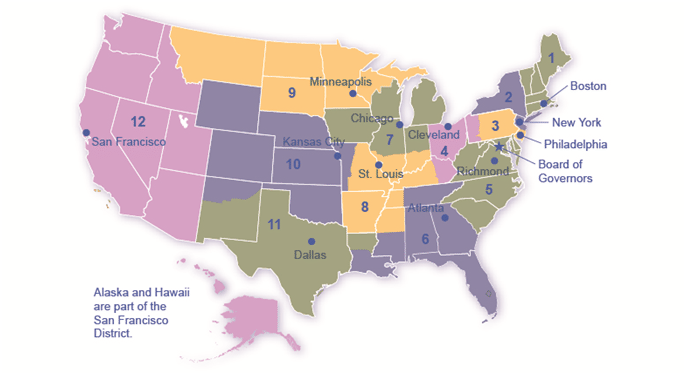

The Federal Reserve is more than the Board of Governors. The Fed also includes 12 regional Federal Reserve banks, each of which is responsible for supporting the commercial banks and economy generally in its district. The Federal Reserve districts and the cities where their regional headquarters are located are shown in Figure 1. The commercial banks in each district elect a Board of Directors for each regional Federal Reserve bank, and that board chooses a president for each regional Federal Reserve district. Thus, the Federal Reserve System includes both federally and private-sector appointed leaders.

The Twelve Federal Reserve Districts

There are twelve regional Federal Reserve banks, each with its district.

Video: What Does a Central Bank Do?

The Federal Reserve

The Federal Reserve, like most central banks, is designed to perform three important functions: to conduct monetary policy that promotes stability of the financial system, to provide banking services to commercial banks and other depository institutions, and to provide banking services to the federal government.

The first two functions are sufficiently important that we will discuss them in their own modules; the third function we will discuss here.

The Federal Reserve provides many of the same services to banks as banks provide to their customers. For example, all commercial banks have an account at the Fed where they deposit reserves. Similarly, banks can obtain loans from the Fed through the “discount window” facility, which will be discussed in more detail later. The Fed is also responsible for check processing. When you write a check, for example, to buy groceries, the grocery store deposits the check in its bank account. Then, the physical check (or an image of that actual check) is returned to your bank, after which funds are transferred from your bank account to the account of the grocery store. The Fed is responsible for each of these actions.

On a more mundane level, the Federal Reserve ensures that enough currency and coins are circulating through the financial system to meet public demands. For example, each year the Fed increases the amount of currency available in banks around the Christmas shopping season and reduces it again in January.

Finally, the Fed is responsible for assuring that banks are in compliance with a wide variety of consumer protection laws. For example, banks are forbidden from discriminating on the basis of age, race, sex, or marital status. Banks are also required to publicly disclose information about the loans they make for buying houses and how those loans are distributed geographically, as well as by sex and race of the loan applicants.

The most prominent task of a central bank is to conduct monetary policy, which involves changes to interest rates and credit conditions, affecting the amount of borrowing and spending in an economy. Some prominent central banks around the world include the U.S. Federal Reserve, the European Central Bank, the Bank of Japan, and the Bank of England.

The Problem of the Zero Percent Interest Rate Lower Bound

Most economists believe that monetary policy (the manipulation of interest rates and credit conditions by a nation’s central bank) has a powerful influence on a nation’s economy. Monetary policy works when the central bank reduces interest rates and makes credit more available. As a result, business investment and other types of spending increase, causing GDP and employment to grow.

But what if the interest rates banks pay are close to zero already? They cannot be made negative, can they? That would mean that lenders pay borrowers for the privilege of taking their money. Yet, this was the situation the U.S. Federal Reserve found itself in at the end of the 2008–2009 recession. The federal funds rate, which is the interest rate for banks that the Federal Reserve targets with its monetary policy, was slightly above 5% in 2007. By 2009, it had fallen to 0.16%.

The Federal Reserve’s situation was further complicated because fiscal policy, the other major tool for managing the economy, was constrained by fears that the federal budget deficit and the public debt were already too high. What were the Federal Reserve’s options? How could the monetary policy be used to stimulate the economy? The answer, as we will see in this chapter, was to change the rules of the game.

Money, loans, and banks are all tied together. Money is deposited in bank accounts, which is then loaned to businesses, individuals, and other banks. When the interlocking system of money, loans, and banks works well, economic transactions are made smoothly in goods and labor markets and savers are connected with borrowers. If the money and banking system does not operate smoothly, the economy can either fall into recession or suffer prolonged inflation.

The government of every country has public policies that support the system of money, loans, and banking, but these policies do not always work perfectly. This chapter discusses how monetary policy works and what may prevent it from working perfectly.

How a Central Bank Executes Monetary Policy

The most important function of the Federal Reserve is to conduct the nation’s monetary policy. Article I, Section 8 of the U.S. Constitution gives Congress the power “to coin money” and “to regulate the value thereof.” As part of the 1913 legislation that created the Federal Reserve, Congress delegated these powers to the Fed. Monetary policy involves managing interest rates and credit conditions, which influences the level of economic activity, as described in more detail below.

A central bank has three traditional tools to implement monetary policy in the economy:

Open market operations

Changing reserve requirements

Changing the discount rate

In discussing how these three tools work, it is useful to think of the central bank as a “bank for banks”—that is, each private-sector bank has its own account at the central bank. We will discuss each of these monetary policy tools in the sections below.

Open Market Operations

The most commonly used tool of monetary policy in the U.S. is open market operations. Open market operations take place when the central bank sells or buys U.S. Treasury bonds in order to influence the quantity of bank reserves and the level of interest rates. The specific interest rate targeted in open market operations is the federal funds rate. The name is a bit of a misnomer since the federal funds rate is the interest rate charged by commercial banks making overnight loans to other banks. As such, it is a very short term interest rate, but one that reflects credit conditions in financial markets very well.

The Federal Open Market Committee (FOMC) makes the decisions regarding these open market operations. The FOMC is made up of the seven members of the Federal Reserve’s Board of Governors. It also includes five voting members who are drawn, on a rotating basis, from the regional Federal Reserve Banks. The New York district president is a permanent voting member of the FOMC and the other four spots are filled on a rotating, annual basis, from the other 11 districts. The FOMC typically meets every six weeks, but it can meet more frequently if necessary. The FOMC tries to act by consensus; however, the chairman of the Federal Reserve has traditionally played a very powerful role in defining and shaping that consensus. For the Federal Reserve, and for most central banks, open market operations have, over the last few decades, been the most commonly used tool of monetary policy.

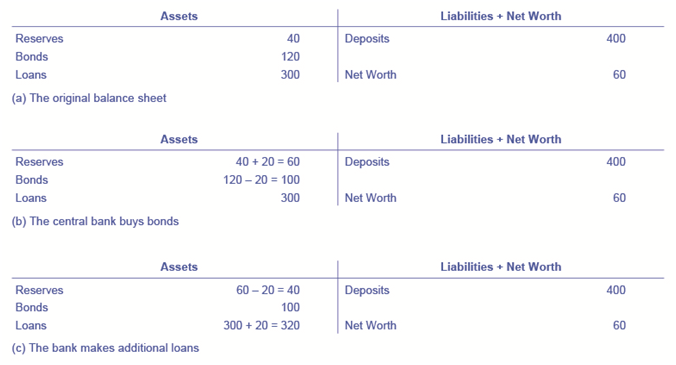

To understand how open market operations affect the money supply, consider the balance sheet of Happy Bank, displayed in Figure 3. Figure 3 (a) shows that Happy Bank starts with $460 million in assets, divided among reserves, bonds and loans, and $400 million in liabilities in the form of deposits, with a net worth of $60 million. When the central bank purchases $20 million in bonds from Happy Bank, the bond holdings of Happy Bank fall by $20 million and the bank’s reserves rise by $20 million, as shown in Figure 3 (b). However, Happy Bank only wants to hold $40 million in reserves (the quantity of reserves that it started with in Figure 3) (a), so the bank decides to loan out the extra $20 million in reserves and its loans rise by $20 million, as shown in Figure 3 (c). The open market operation by the central bank causes Happy Bank to make loans instead of holding its assets in the form of government bonds, which expands the money supply. As the new loans are deposited in banks throughout the economy, these banks will, in turn, loan out some of the deposits they receive, triggering the money multiplier.

Where did the Federal Reserve get the $20 million that it used to purchase the bonds? A central bank has the power to create money. In practical terms, the Federal Reserve would write a check to Happy Bank, so that Happy Bank can have that money credited to its bank account at the Federal Reserve. In truth, the Federal Reserve created the money to purchase the bonds out of thin air—or with a few clicks on some computer keys.

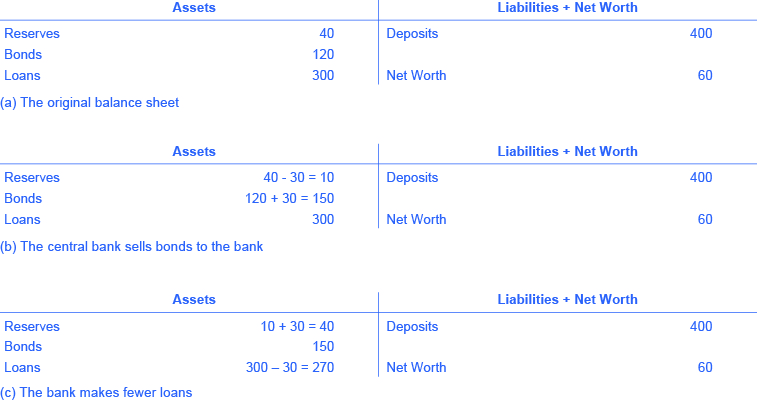

Open market operations can also reduce the quantity of money and loans in an economy. Figure (a) shows the balance sheet of Happy Bank before the central bank sells bonds in the open market. When Happy Bank purchases $30 million in bonds, Happy Bank sends $30 million of its reserves to the central bank, but now holds an additional $30 million in bonds, as shown in Figure (b). However, Happy Bank wants to hold $40 million in reserves, as in Figure (a), so it will adjust down the quantity of its loans by $30 million, to bring its reserves back to the desired level, as shown in Figure (c). In practical terms, a bank can easily reduce its quantity of loans. At any given time, a bank is receiving payments on loans that it made previously and also making new loans. If the bank just slows down or briefly halts making new loans, and instead adds those funds to its reserves, then its overall quantity of loans will decrease. A decrease in the quantity of loans also means fewer deposits in other banks, and other banks reducing their lending as well, as the money multiplier discussed in Money and Banking takes effect. And what about all those bonds? How do they affect the money supply?

Changing Reserve Requirements

A second method of conducting monetary policy is for the central bank to raise or lower the reserve requirement, which, as we noted earlier, is the percentage of each bank’s deposits that it is legally required to hold either as cash in their vault or on deposit with the central bank. If banks are required to hold a greater amount in reserves, they have less money available to lend out. If banks are allowed to hold a smaller amount in reserves, they will have a greater amount of money available to lend out.

In early 2015, the Federal Reserve required banks to hold reserves equal to 0% of the first $14.5 million in deposits, then to hold reserves equal to 3% of the deposits up to $103.6 million, and 10% of any amount above $103.6 million. Small changes in the reserve requirements are made almost every year. For example, the $103.6 million dividing line is sometimes bumped up or down by a few million dollars. In practice, large changes in reserve requirements are rarely used to execute monetary policy. A sudden demand that all banks increase their reserves would be extremely disruptive and difficult to comply with, while loosening requirements too much would create a danger of banks being unable to meet the demand for withdrawals.

Changing the Discount Rate

The Federal Reserve was founded in the aftermath of the Financial Panic of 1907 when many banks failed as a result of bank runs. As mentioned earlier, since banks make profits by lending out their deposits, no bank, even those that are not bankrupt, can withstand a bank run. As a result of the Panic, the Federal Reserve was founded to be the “lender of last resort.” In the event of a bank run, sound banks, (banks that were not bankrupt) could borrow as much cash as they needed from the Fed’s discount “window” to quell the bank run. The interest rate banks pay for such loans is called the discount rate. (They are so named because loans are made against the bank’s outstanding loans “at a discount” of their face value.) Once depositors became convinced that the bank would be able to honor their withdrawals, they no longer had a reason to make a run on the bank. In short, the Federal Reserve was originally intended to provide credit passively, but in the years since its founding, the Fed has taken on a more active role with monetary policy.

So, the third traditional method for conducting monetary policy is to raise or lower the discount rate. If the central bank raises the discount rate, then commercial banks will reduce their borrowing of reserves from the Fed, and instead call in loans to replace those reserves. Since fewer loans are available, the money supply falls and market interest rates rise. If the central bank lowers the discount rate it charges to banks, the process works in reverse.

In recent decades, the Federal Reserve has made relatively few discount loans. Before a bank borrows from the Federal Reserve to fill out its required reserves, the bank is expected to first borrow from other available sources, like other banks. This is encouraged by Fed’s charging a higher discount rate, than the federal funds rate. Given that most banks borrow little at the discount rate, changing the discount rate up or down has little impact on their behavior. More importantly, the Fed has found from experience that open market operations are a more precise and powerful means of executing any desired monetary policy.

In the Federal Reserve Act, the phrase “...to afford means of rediscounting commercial paper” is contained in its long title. This tool was seen as the main tool for monetary policy when the Fed was initially created. This illustrates how monetary policy has evolved and how it continues to do so.

A central bank has three traditional tools to conduct monetary policy: open market operations, which involves buying and selling government bonds with banks; reserve requirements, which determine what level of reserves a bank is legally required to hold; and discount rates, which is the interest rate charged by the central bank on the loans that it gives to other commercial banks. The most commonly used tool is open market operations.

Check It Out: The History of Money Explained in One Infographic

Video: Regulation Z

Video unavailable

Answer the self check questions below to monitor your understanding of the concepts in this section.

Answer the self check questions below to monitor your understanding of the concepts in this section.Self Check Questions

- What is the purpose of the Federal Reserve System?

- What do the Federal Reserve District Banks do?

- What is the main role of the Federal Open Market Committee (FOMC)?

- What is the role of the Federal Reserve in dealing with State Member Banks?

- Name 2 other roles of the Federal Reserve System.

| Image | Reference | Attributions |

|

[Figure 3] | Credit: opentextbc.ca Source: opentextbc.ca/principlesofeconomics/chapter/28-3-how-a-central-bank-executes-monetary-policy/ License: CC BY-NC 3.0 |

|

[Figure 4] | Credit: opentextbc.ca Source: opentextbc.ca/principlesofeconomics/chapter/28-3-how-a-central-bank-executes-monetary-policy/ License: CC BY-NC 3.0 |