2.9: Competition and Market Structures

- Page ID

- 6768

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Competition and Market Structures

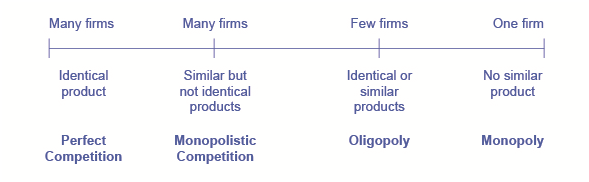

Market structures describe the nature or degree of competition among companies, in the same industries, in a free enterprise economy. Economists have developed a theoretical model of an ideal situation where “perfect competition” occurs. Of course, this is only a model to compare to other types of market structures that are not “perfect”.

For there to be “perfect competition” certain conditions must prevail in the market such as:

- a large number of buyers and sellers,

- they must deal in identical products,

- buyers and sellers act independently and compete with each other,

- both buyers and sellers must be well informed of the conditions in the markets, and

- both buyers and sellers can enter into and leave the market whenever they choose.

So as you may have determined from the five conditions that must exist to have “perfect competition,” there really is no such thing. If any of the five conditions are not met, then the market structure is called “imperfect”.

There are three “imperfect markets”: monopolistic competition, oligopoly, and monopoly.

Universal Generalizations

- Perfect competition is a theory used to evaluate other types of markets.

- There are four basic types of market structures: perfect, monopolistic, oligopoly, and monopoly.

- The type of market structure is determined by the amount of competition among firms operating in the same industry.

- Competition in the marketplace affects price, demand, and supply of goods and services.

Guiding Questions

- How do changes in prices affect demand for goods and/or services for each type of market structure?

- Why does the government allow for monopolies to exist?

- To what extent should the government be involved in the free enterprise market?

Video: Market Structures

Market Structures

Firms behave in much the same way as consumers behave. What does that mean? Let’s define what is meant by the firm. A firm (or business) combines inputs of labor, capital, land, and raw or finished component materials to produce outputs. If the firm is successful, the outputs are more valuable than the inputs. This activity of production goes beyond manufacturing (i.e., making things). It includes any process or service that creates value, including transportation, distribution, wholesale and retail sales. Production involves a number of important decisions that define the behavior of firms. These decisions include, but are not limited to:

- What product or products should the firm produce?

- How should the products be produced (i.e., what production process should be used)?

- How much output should the firm produce?

- What price should the firm charge for its products?

- How much labor should the firm employ?

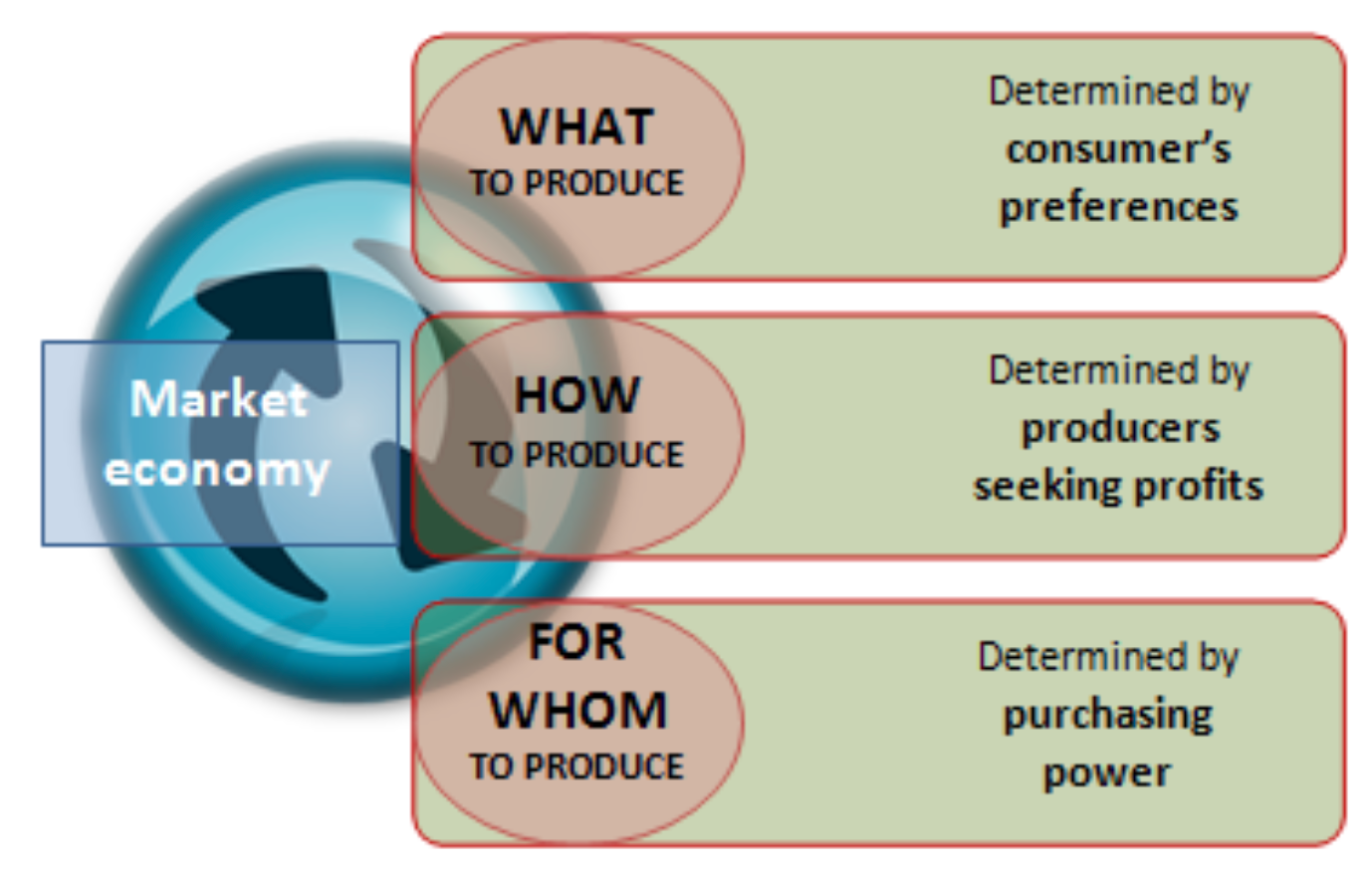

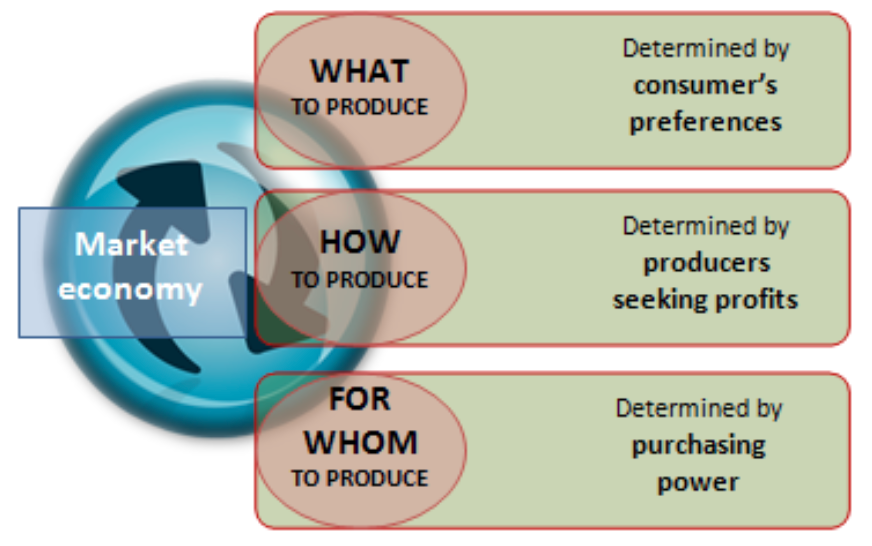

Three Economic Questions

In order to meet the needs of its people, every society must answer three basic economic questions:

- What should we produce?

- How should we produce it?

- For whom should we produce it?

A society (or country) might decide to produce candy or cars, computers or combat boots. The goods might be produced by unskilled workers in privately owned factories or by technical experts in government-funded laboratories. Once they are made, the goods might be given out for free to the poor or sold at high prices that only the rich can afford. The possibilities are endless.

Although every society answers the three basic economic questions differently, in doing so, each confronts the same fundamental problems: resource allocation and scarcity.

Resources are all of the ingredients needed for production, including physical materials (such as land, coal, or timber), labor (workers), technology (not just computers but, in a broader sense, all the technical ability and knowledge that is necessary to produce a given commodity), and capital (the machinery and tools of production). Scarcity refers to the essential fact that people’s wants or desires are always going to be greater than the resources available to fulfill those wants.

Simply put, scarcity means that resources are limited. No country can produce everything, no matter how rich its mines, how massive its forests, or how advanced its technology. Because of the constraints of scarcity, then, decisions must be made about resource allocation (that is, how best to allocate, or distribute, resources for the maximum benefit of the society).

Source: "Three Economic Questions: What, How, For Whom?." Everyday Finance: Economics, Personal Money Management, and Entrepreneurship. Retrieved June 13, 2018 from Encyclopedia.com: http://www.encyclopedia.com/finance/...-what-how-whom

The answers to these questions depend on the production and cost conditions facing each firm. The answers also depend on the structure of the market for the product(s) in question. Market structure is a multidimensional concept that involves how competitive the industry is. It is defined by questions such as these:

- How much market power does each firm in the industry possess?

- How similar is each firm’s product to the products of other firms in the industry?

- How difficult is it for new firms to enter the industry?

- Do firms compete on the basis of price, advertising, or other product differences?

Figure 2 illustrates the range of different market structures

Firms face different competitive situations. At one extreme—perfect competition—many firms are all trying to sell identical products. At the other extreme—monopoly—only one firm is selling the product, and this firm faces no competition. Monopolistic competition and oligopoly fall between the extremes of perfect competition and monopoly. Monopolistic competition is a situation with many firms selling similar, but not identical, products. Oligopoly is a situation with few firms that sell identical or similar products.

In less than two decades, Amazon.com has transformed the way books are sold, bought, and even read. Prior to Amazon, books were primarily sold through independent bookstores with limited inventories in small retail locations. There were exceptions, of course; Borders and Barnes & Noble offered larger stores in urban areas. In the last decade, however, independent bookstores have become few and far between, Borders has gone out of business, and Barnes & Noble is struggling. Online delivery and purchase of books has indeed overtaken the more traditional business models. How has Amazon changed the book selling industry? How has it managed to crush its competition?

A major reason for the giant retailer’s success is its production model and cost structure, which has enabled Amazon to undercut the prices of its competitors even when factoring in the cost of shipping. Read on to see how firms great (like Amazon) and small (like your corner deli) determine what to sell, at what output and price.

Traditionally, bookstores have operated in retail locations with inventories held either on the shelves or in the back of the store. These retail locations were very pricey in terms of rent. Amazon has no retail locations; it sells online and delivers by mail. Amazon offers almost any book in print, convenient purchasing, and prompt delivery by mail. Amazon holds its inventories in huge warehouses in low-rent locations around the world. The warehouses are highly computerized using robots and relatively low-skilled workers, making for low average costs per sale. Amazon demonstrates the significant advantages economies of scale can offer to a firm that exploits those economies.

Perfect Competition and Why It Matters

Firms are said to be in perfect competition when the following conditions occur: (1) many firms produce identical products; (2) many buyers are available to buy the product, and many sellers are available to sell the product; (3) sellers and buyers have all relevant information to make rational decisions about the product being bought and sold; and (4) firms can enter and leave the market without any restrictions—in other words, there is free entry and exit into and out of the market.

A perfectly competitive firm is known as a price taker because the pressure of competing firms forces them to accept the prevailing equilibrium price in the market. If a firm in a perfectly competitive market raises the price of its product by so much as a penny, it will lose all of its sales to competitors. When a wheat grower, as discussed in the Bring it Home feature, wants to know what the going price of wheat is, he or she has to go to the computer or listen to the radio to check. The market price is determined solely by supply and demand in the entire market and not the individual farmer. Also, a perfectly competitive firm must be a very small player in the overall market, so that it can increase or decrease output without noticeably affecting the overall quantity supplied and price in the market.

A perfectly competitive market is a hypothetical extreme; however, producers in a number of industries do face many competitor firms selling highly similar goods, in which case they must often act as price takers. Agricultural markets are often used as an example. The same crops grown by different farmers are largely interchangeable. According to the United States Department of Agriculture monthly reports, in 2012, U.S. corn farmers received an average price of $6.07 per bushel and wheat farmers received an average price of $7.60 per bushel. A corn farmer who attempted to sell at $7.00 per bushel, or a wheat grower who attempted to sell for $8.00 per bushel would not have found any buyers. A perfectly competitive firm will not sell below the equilibrium price either. Why should they when they can sell all they want at the higher price? Other examples of agricultural markets that operate in close to perfectly competitive markets are small roadside produce markets and small organic farmers.

This chapter examines how profit-seeking firms decide how much to produce in perfectly competitive markets. In the short run, the perfectly competitive firm will seek the quantity of output where profits are highest or, if profits are not possible, where losses are lowest. In this example, the “short run” refers to a situation in which firms are producing with one fixed input and incur fixed costs of production. (In the real world, firms can have many fixed inputs.)

In the long run, perfectly competitive firms will react to profits by increasing production. They will respond to losses by reducing production or exiting the market. Ultimately, a long-run equilibrium will be attained when no new firms want to enter the market and existing firms do not want to leave the market, as economic profits have been driven down to zero.

How Perfectly Competitive Firms Make Output Decisions

A perfectly competitive firm has only one major decision to make—namely, what quantity to produce. To understand why this is so, consider a different way of writing out the basic definition of profit:

Profit=Total revenue−Total cost

=(Price)(Quantity produced)−(Average cost)(Quantity produced)

Since a perfectly competitive firm must accept the price for its output as determined by the product’s market demand and supply, it cannot choose the price it charges. This is already determined in the profit equation, and so the perfectly competitive firm can sell any number of units at exactly the same price. It implies that the firm faces a perfectly elastic demand curve for its product: buyers are willing to buy any number of units of output from the firm at the market price. When the perfectly competitive firm chooses what quantity to produce, then this quantity—along with the prices prevailing in the market for output and inputs—will determine the firm’s total revenue, total costs, and ultimately, level of profits.

Determining the Highest Profit by Comparing Total Revenue and Total Cost

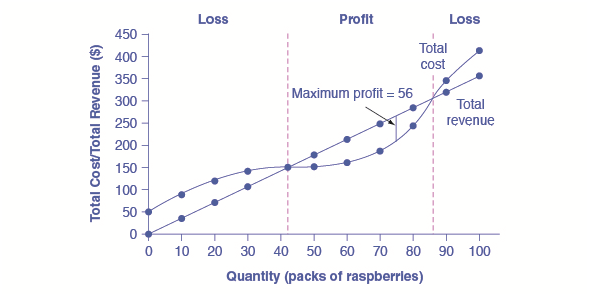

A perfectly competitive firm can sell as large a quantity as it wishes, as long as it accepts the prevailing market price. Total revenue is going to increase as the firm sells more, depending on the price of the product and the number of units sold. If you increase the number of units sold at a given price, then total revenue will increase. If the price of the product increases for every unit sold, then total revenue also increases. As an example of how a perfectly competitive firm decides what quantity to produce, consider the case of a small farmer who produces raspberries and sells them frozen for $4 per pack. Sales of one pack of raspberries will bring in $4, two packs will be $8, three packs will be $12, and so on. If, for example, the price of frozen raspberries doubles to $8 per pack, then sales of one pack of raspberries will be $8, two packs will be $16, three packs will be $24, and so on.

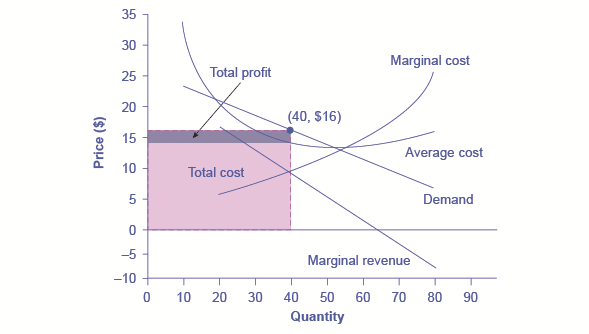

Total revenue and total costs for the raspberry farm, broken down into fixed and variable costs, are shown in Table 1 and also appear in Figure 3. The horizontal axis shows the quantity of frozen raspberries produced in packs; the vertical axis shows both total revenue and total costs, measured in dollars. The total cost curve intersects with the vertical axis at a value that shows the level of fixed costs, and then slopes upward.

Total Cost and Total Revenue at the Raspberry Farm

Total revenue for a perfectly competitive firm is a straight line sloping up. The slope is equal to the price of the good. Total cost also slopes up, but with some curvature. At higher levels of output, total cost begins to slope upward more steeply because of diminishing marginal returns. The maximum profit will occur at the quantity where the gap of total revenue over total cost is largest.

| Quantity | Total Cost | Fixed Cost | Variable Cost | Total Revenue | Profit |

| (Q) | (TC) | (FC) | (VC) | (TR) | |

| 0 | $62 | $62 | - | $0 | −$62 |

| 10 | $90 | $62 | $28 | $40 | −$50 |

| 20 | $110 | $62 | $48 | $80 | −$30 |

| 30 | $126 | $62 | $64 | $120 | −$6 |

| 40 | $144 | $62 | $82 | $160 | $16 |

| 50 | $166 | $62 | $104 | $200 | $34 |

| 60 | $192 | $62 | $130 | $240 | $48 |

| 70 | $224 | $62 | $162 | $280 | $56 |

| 80 | $264 | $62 | $202 | $320 | $56 |

| 90 | $324 | $62 | $262 | $360 | $36 |

| 100 | $404 | $62 | $342 | $400 | −$4 |

Based on its total revenue and total cost curves, a perfectly competitive firm like the raspberry farm can calculate the quantity of output that will provide the highest level of profit. At any given quantity, total revenue minus total cost will equal profit. One way to determine the most profitable quantity to produce is to see at what quantity total revenue exceeds total cost by the largest amount. In Figure 3, the vertical gap between total revenue and total cost represents either profit (if total revenues are greater than total costs at a certain quantity) or losses (if total costs are greater than total revenues at a certain quantity). In this example, total costs will exceed total revenues at output levels from 0 to 40, and so over this range of output, the firm will be making losses. At output levels from 50 to 80, total revenues exceed total costs, so the firm is earning profits. But then at an output of 90 or 100, total costs again exceed total revenues and the firm is making losses. The highest total profits in the figure, occur at an output of 70–80, when profits will be $56.

A higher price would mean that total revenue would be higher for every quantity sold. A lower price would mean that total revenue would be lower for every quantity sold. What happens if the price drops low enough so that the total revenue line is completely below the total cost curve; that is, at every level of output, total costs are higher than total revenues? In this instance, the best the firm can do is to suffer losses. But a profit-maximizing firm will prefer the quantity of output where total revenues come closest to total costs and thus where the losses are smallest.

Entry and Exit Decisions in the Long Run

The line between the short run and the long run cannot be defined precisely with a stopwatch or even with a calendar. It varies according to the specific business. The distinction between the short run and the long run is, therefore, more technical: in the short run, firms cannot change the usage of fixed inputs, while in the long run, the firm can adjust all factors of production.

In a competitive market, profits are a red cape that incite businesses to charge. If a business is making a profit in the short run, it has an incentive to expand existing factories or to build new ones. New firms may start production, as well. When new firms enter the industry in response to increased industry profits it is called entry.

Losses are the black thundercloud that causes businesses to flee. If a business is making losses in the short run, it will either keep limping along or just shut down, depending on whether its revenues are covering its variable costs. But in the long run, firms that are facing losses will shut down at least some of their output, and some firms will cease production altogether. The long run process of reducing production in response to a sustained pattern of losses is called exit. The following Clear It Up feature discusses where some of these losses might come from, and the reasons why some firms go out of business.

Why do Firms Cease to Exist?

Can we say anything about what causes a firm to exit an industry? Profits are the measurement that determines whether a business stays operating or not. Individuals start businesses with the purpose of making profits. They invest their money, time, effort, and many other resources to produce and sell something that they hope will give them something in return. Unfortunately, not all businesses are successful, and many new startups soon realize that their “business adventure” must eventually end.

In the model of perfectly competitive firms, those that consistently cannot make money will “exit,” which is a nice, bloodless word for a more painful process. When a business fails, after all, workers lose their jobs, investors lose their money, and owners and managers can lose their dreams. Many businesses fail. The U.S. Small Business Administration indicates that in 2009–2010, for example, 533,945 firms “entered” in the United States, but 593,347 firms “exited.” About 96.3% and 96.6% of these business entries and exits, respectively, involved small firms with fewer than 20 employees.

Sometimes a business fails because of poor management or workers who are not very productive, or because of tough domestic or foreign competition. Businesses also fail from a variety of causes that might best be summarized as bad luck. For example, conditions of demand and supply in the market shift in an unexpected way, so that the prices that can be charged for outputs fall or the prices that need to be paid for inputs rise. With millions of businesses in the U.S. economy, even a small fraction of them failing will affect many people—and business failures can be very hard on the workers and managers directly involved. But from the standpoint of the overall economic system, business exits are sometimes a necessary evil if a market-oriented system is going to offer a flexible mechanism for satisfying customers, keeping costs low, and inventing new products.

Video: Comparing Market Structures

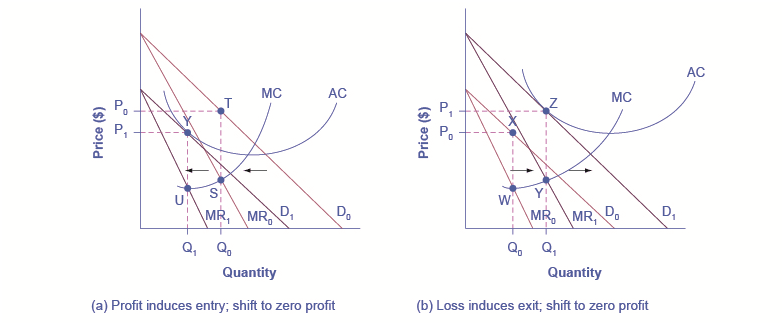

How Entry and Exit Lead to Zero Profits in the Long Run

No perfectly competitive firm acting alone can affect the market price. However, the combination of many firms entering or exiting the market will affect overall supply in the market. In turn, a shift in supply for the market as a whole will affect the market price. Entry and exit to and from the market are the driving forces behind a process that, in the long run, pushes the price down to minimum average total costs so that all firms are earning a zero profit.

To understand how short-run profits for a perfectly competitive firm will evaporate in the long run, imagine the following situation. The market is in long-run equilibrium, where all firms earn zero economic profits producing the output level where P = MR = MC and P = AC. No firm has the incentive to enter or leave the market. Let’s say that the product’s demand increases, and with that, the market price goes up. The existing firms in the industry are now facing a higher price than before, so they will increase production to the new output level where P = MR = MC.

This will temporarily make the market price rise above the average cost curve, and therefore, the existing firms in the market will now be earning economic profits. However, these economic profits attract other firms to enter the market. Entry of many new firms causes the market supply curve to shift to the right. As the supply curve shifts to the right, the market price starts decreasing, and with that, economic profits fall for new and existing firms. As long as there are still profits in the market, entry will continue to shift supply to the right. This will stop whenever the market price is driven down to the zero-profit level, where no firm is earning economic profits.

Short run losses will fade away by reversing this process. Say that the market is in long run equilibrium. This time, demand decreases, and with that, the market price starts falling. The existing firms in the industry are now facing a lower price than before, and as it will be below the average cost curve, they will now be making economic losses. Some firms will continue producing where the new P = MR = MC, as long as they are able to cover their average variable costs. Some firms will have to shut down immediately as they will not be able to cover their average variable costs, and then will only incur their fixed costs, minimizing their losses. Exit of many firms causes the market supply curve to shift to the left. As the supply curve shifts to the left, the market price starts rising, and economic losses start to be lower. This process ends whenever the market price rises to the zero-profit level, where the existing firms are no longer losing money and are at zero profits again. Thus, while a perfectly competitive firm can earn profits in the short run, in the long run the process of entry will push down prices until they reach the zero-profit level. Conversely, while a perfectly competitive firm may earn losses in the short run, firms will not continually lose money. In the long run, firms making losses are able to escape from their fixed costs, and their exit from the market will push the price back up to the zero-profit level. In the long run, this process of entry and exit will drive the price in perfectly competitive markets to the zero-profit point at the bottom of the AC curve, where marginal cost crosses average cost.

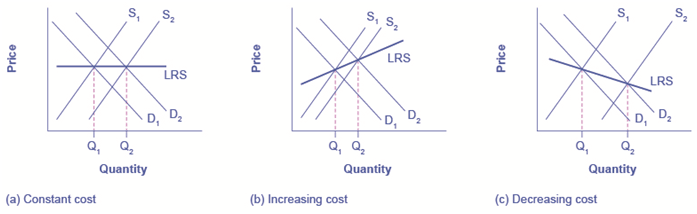

The Long Run Adjustment and Industry Types

Whenever there are expansions in an industry, costs of production for the existing and new firms could either stay the same, increase, or even decrease. Therefore, we can categorize an industry as being (1) a constant cost industry (as demand increases, the cost of production for firms stays the same), (2) an increasing cost industry (as demand increases, the cost of production for firms increases), or (3) a decreasing cost industry (as demand increases the costs of production for the firms decreases).

For a constant cost industry, whenever there is an increase in market demand and price, then the supply curve shifts to the right with new firms’ entry and stops at the point where the new long-run equilibrium intersects at the same market price as before. But why will costs remain the same? In this type of industry, the supply curve is very elastic. Firms can easily supply any quantity that consumers demand. In addition, there is a perfectly elastic supply of inputs—firms can easily increase their demand for employees, for example, with no increase to wages. Tying in to our Bring it Home discussion, an increased demand for ethanol in recent years has caused the demand for corn to increase. Consequently, many farmers switched from growing wheat to growing corn. Agricultural markets are generally good examples of constant cost industries.

For an increasing cost industry, as the market expands, the old and new firms experience increases in their costs of production, which makes the new zero-profit level intersect at a higher price than before. Here companies may have to deal with limited inputs, such as skilled labor. As the demand for these workers rise, wages rise and this increases the cost of production for all firms. The industry supply curve in this type of industry is more inelastic.

For a decreasing cost industry, as the market expands, the old and new firms experience lower costs of production, which makes the new zero-profit level intersect at a lower price than before. In this case, the industry and all the firms in it are experiencing falling average total costs. This can be due to an improvement in technology in the entire industry or an increase in the education of employees. High tech industries may be a good example of a decreasing cost market.

Figure 4 (a) presents the case of an adjustment process in a constant cost industry. Whenever there are output expansions in this type of industry, the long-run outcome implies more output produced at exactly the same original price. Note that supply was able to increase to meet the increased demand. When we join the before and after long-run equilibriums, the resulting line is the long run supply (LRS) curve in perfectly competitive markets. In this case, it is a flat curve. Figure 4(b) and Figure 4 (c) present the cases for an increasing cost and decreasing cost industry, respectively. For an increasing cost industry, the LRS is upward sloping, while for a decreasing cost industry, the LRS is downward sloping.

Adjustment Process in a Constant-Cost Industry

In (a), demand increased and supply met it. Notice that the supply increase is equal to the demand increase. The result is that the equilibrium price stays the same as quantity sold increases. In (b), notice that sellers were not able to increase supply as much as demand. Some inputs were scarce, or wages were rising. The equilibrium price rises. In (c), sellers easily increased supply in response to the demand increase. Here, new technology or economies of scale caused the large increase in supply, resulting in declining equilibrium price.

Efficiency in Perfectly Competitive Markets

When profit-maximizing firms in perfectly competitive markets combine with utility-maximizing consumers, something remarkable happens: the resulting quantities of outputs of goods and services demonstrate both productive and allocative efficiency.

Productive efficiency means producing without waste, so that the choice is on the production possibility frontier. In the long run in a perfectly competitive market, because of the process of entry and exit, the price in the market is equal to the minimum of the long-run average cost curve. In other words, goods are being produced and sold at the lowest possible average cost.

Allocative efficiency means that among the points on the production possibility frontier, the point that is chosen is socially preferred—at least in a particular and specific sense. In a perfectly competitive market, price will be equal to the marginal cost of production. Think about the price that is paid for a good as a measure of the social benefit received for that good; after all, willingness to pay conveys what the good is worth to a buyer. Then think about the marginal cost of producing the good as representing not just the cost for the firm, but more broadly as the social cost of producing that good. When perfectly competitive firms follow the rule that profits are maximized by producing at the quantity where price is equal to marginal cost, they are thus ensuring that the social benefits received from producing a good are in line with the social costs of production.

To explore what is meant by allocative efficiency, it is useful to walk through an example. Begin by assuming that the market for wholesale flowers is perfectly competitive, and so P = MC. Now, consider what it would mean if firms in that market produced a lesser quantity of flowers. At a lesser quantity, marginal costs will not yet have increased as much, so that price will exceed marginal cost; that is, P > MC. In that situation, the benefit to society as a whole of producing additional goods, as measured by the willingness of consumers to pay for marginal units of a good, would be higher than the cost of the inputs of labor and physical capital needed to produce the marginal good. In other words, the gains to society as a whole from producing additional marginal units will be greater than the costs.

Conversely, consider what it would mean if, compared to the level of output at the allocatively efficient choice when P = MC, firms produced a greater quantity of flowers. At a greater quantity, marginal costs of production will have increased so that P < MC. In that case, the marginal costs of producing additional flowers is greater than the benefit to society as measured by what people are willing to pay. For society as a whole, since the costs are outstripping the benefits, it will make sense to produce a lower quantity of such goods.

When perfectly competitive firms maximize their profits by producing the quantity where P = MC, they also assure that the benefits to consumers of what they are buying, as measured by the price they are willing to pay, is equal to the costs to society of producing the marginal units, as measured by the marginal costs the firm must pay—and thus that allocative efficiency holds.

The statements that a perfectly competitive market in the long run will feature both productive and allocative efficiency do need to be taken with a few grains of salt. Remember, economists are using the concept of “efficiency” in a particular and specific sense, not as a synonym for “desirable in every way.” For one thing, consumers’ ability to pay reflects the income distribution in a particular society. Thus, a homeless person may have no ability to pay for housing because they have insufficient income.

Perfect competition, in the long run, is a hypothetical benchmark. For market structures such as monopoly, monopolistic competition, and oligopoly, which are more frequently observed in the real world than perfect competition, firms will not always produce at the minimum of average cost, nor will they always set price equal to marginal cost. Thus, these other competitive situations will not produce productive and allocative efficiency.

Moreover, real-world markets include many issues that are assumed away in the model of perfect competition, including pollution, inventions of new technology, poverty which may make some people unable to pay for basic necessities of life, government programs like national defense or education, discrimination in labor markets, and buyers and sellers who must deal with imperfect and unclear information. These issues are explored in other chapters. However, the theoretical efficiency of perfect competition does provide a useful benchmark for comparing the issues that arise from these real-world problems.

Monopoly

There is a widespread belief that top executives at firms are the strongest supporters of market competition, but this belief is far from the truth. Think about it this way: If you very much wanted to win an Olympic gold medal, would you rather be far better than everyone else, or locked in competition with many athletes just as good as you are? Similarly, if you would like to attain a very high level of profits, would you rather manage a business with little or no competition, or struggle against many tough competitors who are trying to sell to your customers?

If perfect competition is a market where firms have no market power and they simply respond to the market price, monopoly is a market with no competition at all, and firms have complete market power. In the case of monopoly, one firm produces all of the output in a market. Since a monopoly faces no significant competition, it can charge any price it wishes. While a monopoly, by definition, refers to a single firm, in practice the term is often used to describe a market in which one firm merely has a very high market share. This tends to be the definition that the U.S. Department of Justice uses.

Even though there are very few true monopolies in existence, we do deal with some of those few every day, often without realizing it: The U.S. Postal Service, your electric and garbage collection companies are a few examples. Some new drugs are produced by only one pharmaceutical firm—and no close substitutes for that drug may exist.

From the mid-1990s until 2004, the U.S. Department of Justice prosecuted the Microsoft Corporation for including Internet Explorer as the default web browser with its operating system. The Justice Department’s argument was that, since Microsoft possessed an extremely high market share in the industry for operating systems, the inclusion of a free web browser constituted unfair competition to other browsers, such as Netscape Navigator. Since nearly everyone was using Windows, including Internet Explorer eliminated the incentive for consumers to explore other browsers and made it impossible for competitors to gain a foothold in the market. In 2013, the Windows system ran on more than 90% of the most commonly sold personal computers.

Monopolies are protected from competition, including laws that prohibit competition, technological advantages, and certain configurations of demand and supply. It then discusses how a monopoly will choose its profit-maximizing quantity to produce and what price to charge. While a monopoly must be concerned about whether consumers will purchase its products or spend their money on something altogether different, the monopolist need not worry about the actions of other competing firms producing its products. As a result, a monopoly is not a price taker like a perfectly competitive firm, but instead exercises some power to choose its market price.

Video: Monopolies and Anti-Competitive Markets

How Monopolies Form: Barriers to Entry

Because of the lack of competition, monopolies tend to earn significant economic profits. These profits should attract vigorous competition, and yet, because of one particular characteristic of monopoly, they do not. Barriers to entry are the legal, technological, or market forces that discourage or prevent potential competitors from entering a market. Barriers to entry can range from the simple and easily surmountable, such as the cost of renting retail space, to the extremely restrictive. For example, there are a finite number of radio frequencies available for broadcasting. Once the rights to all of them have been purchased, no new competitors can enter the market.

In some cases, barriers to entry may lead to monopoly. In other cases, they may limit competition to a few firms. Barriers may block entry even if the firm or firms currently in the market are earning profits. Thus, in markets with significant barriers to entry, it is not true that abnormally high profits will attract new firms, and that this entry of new firms will eventually cause the price to decline so that surviving firms earn only a normal level of profit in the long run.

There are two types of monopolies based on the types of barriers to entry they exploit. One is natural monopoly where the barriers to entry are something other than legal prohibition. The other is legal monopoly where laws prohibit (or severely limit) competition.

Natural Monopoly

Economies of scale can combine with the size of the market to limit competition. This situation, when economies of scale are large relative to the quantity demanded in the market, is called a natural monopoly. Natural monopolies often arise in industries where the marginal cost of adding an additional customer is very low, once the fixed costs of the overall system are in place. Once the main water pipes are laid through a neighborhood, the marginal cost of providing water service to another home is fairly low. Once electricity lines are installed through a neighborhood, the marginal cost of providing additional electrical service to one more home is very low. It would be costly and duplicative for a second water company to enter the market and invest in a whole second set of main water pipes, or for a second electricity company to enter the market and invest in a whole new set of electrical wires. These industries offer an example where, because of economies of scale, one producer can serve the entire market more efficiently than a number of smaller producers that would need to make duplicate physical capital investments.

A natural monopoly can also arise in smaller local markets for products that are difficult to transport. For example, cement production exhibits economies of scale, and the quantity of cement demanded in a local area may not be much larger than what a single plant can produce. Moreover, the costs of transporting cement over land are high, and so a cement plant in an area without access to water transportation may be a natural monopoly.

Control of a Physical Resource

Another type of natural monopoly occurs when a company has control of a scarce physical resource. In the U.S. economy, one historical example of this pattern occurred when ALCOA—the Aluminum Company of America—controlled most of the supply of bauxite, a key mineral used in making aluminum. Back in the 1930s, when ALCOA controlled most of the bauxite, other firms were simply unable to produce enough aluminum to compete.

As another example, the majority of global diamond production is controlled by DeBeers, a multi-national company that has mining and production operations in South Africa, Botswana, Namibia, and Canada. It also has exploration activities on four continents, while directing a worldwide distribution network of rough diamonds. Though in recent years they have experienced growing competition, their impact on the rough diamond market is still considerable.

Legal Monopoly

For some products, the government erects barriers to entry by prohibiting or limiting competition. Under U.S. law, no organization but the U.S. Postal Service is legally allowed to deliver first-class mail. Many states or cities have laws or regulations that allow households a choice of only one electric company, one water company, and one company to pick up the garbage. Most legal monopolies are considered utilities—products necessary for everyday life—that are socially beneficial to have. As a consequence, the government allows producers to become regulated monopolies, to insure that an appropriate amount of these products is provided to consumers. Additionally, legal monopolies are often subject to economies of scale, so it makes sense to allow only one provider.

Promoting Innovation

Innovation takes time and resources to achieve. Suppose a company invests in research and development and finds the cure for the common cold. In this world of near ubiquitous information, other companies could take the formula, produce the drug, and because they did not incur the costs of research and development (R&D), undercut the price of the company that discovered the drug. Given this possibility, many firms would choose not to invest in research and development, and as a result, the world would have less innovation. To prevent this from happening, the Constitution of the United States specifies in Article I, Section 8: “The Congress shall have Power . . . To Promote the Progress of Science and Useful Arts, by securing for limited Times to Authors and Inventors the Exclusive Right to their Writings and Discoveries.” Congress used this power to create the U.S. Patent and Trademark Office, as well as the U.S. Copyright Office. A patent gives the inventor the exclusive legal right to make, use, or sell the invention for a limited time; in the United States, exclusive patent rights last for 20 years. The idea is to provide limited monopoly power so that innovative firms can recoup their investment in R&D, but then to allow other firms to produce the product more cheaply once the patent expires.

A trademark is an identifying symbol or name for a particular good like Chiquita bananas, Chevrolet cars, or the Nike “swoosh” that appears on shoes and athletic gear. Roughly 1.9 million trademarks are registered with the U.S. government. A firm can renew a trademark over and over again, as long as it remains in active use.

A copyright, according to the U.S. Copyright Office, “is a form of protection provided by the laws of the United States for ‘original works of authorship’ including literary, dramatic, musical, architectural, cartographic, choreographic, pantomimic, pictorial, graphic, sculptural, and audiovisual creations.” No one can reproduce, display, or perform a copyrighted work without permission of the author. Copyright protection ordinarily lasts for the life of the author plus 70 years.

Roughly speaking, patent law covers inventions and copyright protects books, songs, and art. In certain areas, like the invention of new software, it has been unclear whether patent or copyright protection should apply. There is also a body of law known as trade secrets. Even if a company does not have a patent on an invention, competing firms are not allowed to steal their secrets. One famous trade secret is the formula for Coca-Cola, which is not protected under copyright or patent law, but is simply kept secret by the company.

Taken together, this combination of patents, trademarks, copyrights, and trade secret law is called intellectual property because it implies ownership over an idea, concept, or image, not a physical piece of property like a house or a car. Countries around the world have enacted laws to protect intellectual property although the time periods and exact provisions of such laws vary across countries. There are ongoing negotiations, both through the World Intellectual Property Organization (WIPO) and through international treaties, to bring greater harmony to the intellectual property laws of different countries to determine the extent to which patents and copyrights in one country will be respected in other countries.

Government limitations on competition used to be even more common in the United States. For most of the twentieth century, only one phone company—AT&T—was legally allowed to provide local and long distance service. From the 1930s to the 1970s, one set of federal regulations limited which destinations airlines could choose to fly to and what fares they could charge; another set of regulations limited the interest rates that banks could pay to depositors; yet another specified what trucking firms could charge customers.

What products are considered utilities depends, in part, on the available technology. Fifty years ago, local and long distance telephone service was provided over wires. It did not make much sense to have multiple companies building multiple systems of wiring across towns and across the country. AT&T lost its monopoly on long distance service when the technology for providing phone service changed from wires to microwave and satellite transmission, so that multiple firms could use the same transmission mechanism. The same thing happened to local service, especially in recent years, with the growth in cellular phone systems.

The combination of improvements in production technologies and a general sense that the markets could provide services adequately led to a wave of deregulation, starting in the late 1970s and continuing into the 1990s. This wave eliminated or reduced government restrictions on the firms that could enter, the prices that could be charged, and the quantities that could be produced in many industries, including telecommunications, airlines, trucking, banking, and electricity.

Around the world, from Europe to Latin America to Africa and Asia, many governments continue to control and limit competition in what those governments perceive to be key industries, including airlines, banks, steel companies, oil companies, and telephone companies.

Regulating Natural Monopolies

Most true monopolies today in the U.S. are regulated natural monopolies. A natural monopoly poses a difficult challenge for competition policy, because the structure of costs and demand seems to make competition unlikely or costly. A natural monopoly arises when average costs are declining over the range of production that satisfies market demand. This typically happens when fixed costs are large relative to variable costs. As a result, one firm is able to supply the total quantity demanded in the market at lower cost than two or more firms—so splitting up the natural monopoly would raise the average cost of production and force customers to pay more.

Public utilities, the companies that have traditionally provided water and electrical service across much of the United States, are leading examples of natural monopoly. It would make little sense to argue that a local water company should be broken up into several competing companies, each with its own separate set of pipes and water supplies. Installing four or five identical sets of pipes under a city, one for each water company, so that each household could choose its own water provider would be terribly costly. The same argument applies to the idea of having many competing companies for delivering electricity to homes, each with its own set of wires. Before the advent of wireless phones, the argument also applied to the idea of many different phone companies, each with its own set of phone wires running through the neighborhood.

The Choices in Regulating a Natural Monopoly

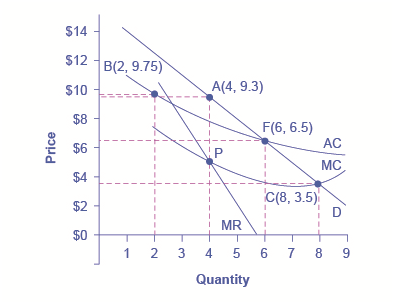

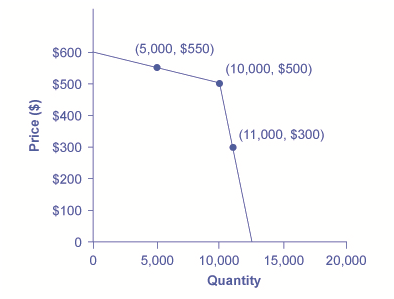

So what is the appropriate competition policy for a natural monopoly? Figure 5 illustrates the case of natural monopoly, with a market demand curve that cuts through the downward-sloping portion of the average cost curve. Points A, B, C, and F illustrate four of the main choices for regulation. Table 2 outlines the regulatory choices for dealing with a natural monopoly.

Regulatory Choices in Dealing with a Natural Monopoly

Figure 4 --A natural monopoly will maximize profits by producing at the quantity where marginal revenue (MR) equals marginal costs (MC) and by then looking to the market demand curve to see what price to charge for this quantity. This monopoly will produce at point A, with a quantity of 4 and a price of 9.3. If antitrust regulators split this company exactly in half, then each half would produce at point B, with average costs of 9.75 and output of 2. The regulators might require the firm to produce where marginal cost crosses the market demand curve at point C. However, if the firm is required to produce at a quantity of 8 and sell at a price of 3.5, the firm will suffer from losses. The most likely choice is point F, where the firm is required to produce a quantity of 6 and charge a price of 6.5.

| Quantity | Price | Total Revenue* | Marginal Revenue | Total Cost | Marginal Cost | Average Cost |

| 1 | 14.7 | 14.7 | - | 11.0 | - | 11.00 |

| 2 | 12.4 | 24.7 | 10.0 | 19.5 | 8.5 | 9.75 |

| 3 | 10.6 | 31.7 | 7.0 | 25.5 | 6.0 | 8.50 |

| 4 | 9.3 | 37.2 | 5.5 | 31.0 | 5.5 | 7.75 |

| 5 | 8.0 | 40.0 | 2.8 | 35.0 | 4.0 | 7.00 |

| 6 | 6.5 | 39.0 | –1.0 | 39.0 | 4.0 | 6.50 |

| 7 | 5.0 | 35.0 | –4.0 | 42.0 | 3.0 | 6.00 |

| 8 | 3.5 | 28.0 | –7.0 | 45.5 | 3.5 | 5.70 |

| 9 | 2.0 | 18.0 | –10.0 | 49.5 | 4.0 | 5.5 |

Regulatory Choices in Dealing with Natural Monopoly(*Total Revenue is given by multiplying price and quantity. However, some of the price values in this table have been rounded for ease of presentation.)

The first possibility is to leave the natural monopoly alone. In this case, the monopoly will follow its normal approach to maximizing profits. It determines the quantity where MR = MC, which happens at point P at a quantity of 4. The firm then looks to point A on the demand curve to find that it can charge a price of 9.3 for that profit-maximizing quantity. Since the price is above the average cost curve, the natural monopoly would earn economic profits.

A second outcome arises if antitrust authorities decide to divide the company, so that the new firms can compete. As a simple example, imagine that the company is cut in half. Thus, instead of one large firm producing a quantity of 4, two half-size firms each produce a quantity of 2. Because of the declining average cost curve (AC), the average cost of production for each of the half-size companies each producing 2, as shown at point B, would be 9.75, while the average cost of production for a larger firm producing 4 would only be 7.75. Therefore, the economy would become less productively efficient since the good is being produced at a higher average cost. In a situation with a downward-sloping average cost curve, two smaller firms will always have higher average costs of production than one larger firm for any quantity of total output. In addition, the antitrust authorities must worry that splitting the natural monopoly into pieces may be only the start of their problems. If one of the two firms grows larger than the other, it will have lower average costs and may be able to drive its competitor out of the market. Alternatively, two firms in a market may discover subtle ways of coordinating their behavior and keeping prices high. Either way, the result will not be the greater competition that was desired.

A third alternative is that regulators may decide to set prices and quantities produced for this industry. The regulators will try to choose a point along the market demand curve that benefits both consumers and the broader social interest. Point C illustrates one tempting choice: the regulator requires that the firm produce the quantity of output where marginal cost crosses the demand curve at an output of 8, and charge the price of 3.5, which is equal to marginal cost at that point. This rule is appealing because it requires price to be set equal to marginal cost, which is what would occur in a perfectly competitive market, and it would assure consumers a higher quantity and lower price than at the monopoly choice A. In fact, efficient allocation of resources would occur at point C, since the value to the consumers of the last unit bought and sold in this market is equal to the marginal cost of producing it.

Attempting to bring about point C through force of regulation, however, runs into a severe difficulty. At point C, with an output of 8, a price of 3.5 is below the average cost of production, which is 5.7, and so if the firm charges a price of 3.5, it will be suffering losses. Unless the regulators or the government offer the firm an ongoing public subsidy (and there are numerous political problems with that option), the firm will lose money and go out of business.

Perhaps the most plausible option for the regulator is point F; that is, to set the price where AC crosses the demand curve at an output of 6 and a price of 6.5. This plan makes some sense at an intuitive level: let the natural monopoly charge enough to cover its average costs and earn a normal rate of profit, so that it can continue operating, but prevent the firm from raising prices and earning abnormally high monopoly profits, as it would at the monopoly choice A. Of course, determining this level of output and price with the political pressures, time constraints, and limited information of the real world is much harder than identifying the point on a graph. For more on the problems that can arise from a centrally determined price, see the discussion of price floors and price ceilings in Demand and Supply.

The Great Deregulation Experiment

Governments at all levels across the United States have regulated prices in a wide range of industries. In some cases, like water and electricity that have natural monopoly characteristics, there is some room in economic theory for such regulation. But once politicians are given a basis to intervene in markets and to choose prices and quantities, it is hard to know where to stop.

Doubts about Regulation of Prices and Quantities

Beginning in the 1970s, it became clear to policymakers of all political leanings that the existing price regulation was not working well. The United States carried out a great policy experiment—the deregulation discussed in Monopoly—removing government controls over prices and quantities produced in airlines, railroads, trucking, intercity bus travel, natural gas, and bank interest rates. The Clear it Up discusses the outcome of deregulation in one industry in particular—airlines.

What are the Results of Airline Deregulation?

Why did the pendulum swing in favor of deregulation? Consider the airline industry. In the early days of air travel, no airline could make a profit just by flying passengers. Airlines needed something else to carry and the Postal Service provided that something with airmail. So the first U.S. government regulation of the airline industry happened through the Postal Service when. In 1926 the Postmaster General began giving airlines permission to fly certain routes based on the needs of mail delivery—and the airlines took some passengers along for the ride. In 1934, the Postmaster General was charged by the antitrust authorities with colluding with the major airlines of that day to monopolize the nation’s airways. In 1938, the Civil Aeronautics Board (CAB) was created to regulate airfares and routes instead. For 40 years, from 1938 to 1978, the CAB approved all fares, controlled all entry and exit, and specified which airlines could fly which routes. There was zero entry of new airlines on the main routes across the country for 40 years because the CAB did not think it was necessary.

In 1978, the Airline Deregulation Act took the government out of the business of determining airfares and schedules. The new law shook up the industry. Famous old airlines like Pan American, Eastern, and Braniff went bankrupt and disappeared. Some new airlines like People Express were created—and then vanished.

The greater competition from deregulation reduced airfares by about one-third over the next two decades, saving consumers billions of dollars a year. The average flight used to take off with just half its seats full; now it is two-thirds full, which is far more efficient. Airlines have also developed hub-and-spoke systems, where planes all fly into a central hub city at a certain time and then depart. As a result, one can fly between any of the spoke cities with just one connection—and there is greater service to more cities than before deregulation. With lower fares and more service, the number of air passengers doubled from the late 1970s to the start of the 2000s—an increase that, in turn, doubled the number of jobs in the airline industry. Meanwhile, with the watchful oversight of government safety inspectors, commercial air travel has continued to grow safer over time.

The U.S. airline industry is far from perfect. For example, a string of mergers in recent years has raised concerns over how competition might be compromised.

One difficulty with government price regulation is what economists call regulatory capture. This occurs when the firms supposedly being regulated end up playing a large role in setting the regulations that they will follow. When the airline industry was being regulated, for example, it suggested appointees to the regulatory board, sent lobbyists to argue with the board, provided most of the information on which the board made decisions, and offered well-paid jobs to at least some of the people leaving the board. In this situation, consumers can easily end up being not very well represented by the regulators. The result of regulatory capture is that government price regulation can often become a way for existing competitors to work together to reduce output, keep prices high, and limit competition.

The Effects of Deregulation

Deregulation, both of airlines and of other industries, has its negatives. The greater pressure of competition led to entry and exit. When firms went bankrupt or contracted substantially in size, they laid off workers who had to find other jobs. Market competition is, after all, a full-contact sport.

A number of major accounting scandals involving prominent corporations such as Enron, Tyco International, and WorldCom led to the Sarbanes-Oxley Act in 2002. Sarbanes-Oxley was designed to increase confidence in financial information provided by public corporations to protect investors from accounting fraud.

The Great Recession which began in late 2007 and which the U.S. economy is still struggling to recover from was caused at least in part by a global financial crisis, which began in the United States. The key component of the crisis was the creation and subsequent failure of several types of unregulated financial assets, such as collateralized mortgage obligations (CMOs, a type of mortgage-backed security), and credit default swaps (CDSs, insurance contracts on assets like CMOs that provided a payoff even if the holder of the CDS did not own the CMO). Many of these assets were rated very safe by private credit rating agencies such as Standard & Poors, Moody’s, and Fitch.

The collapse of the markets for these assets precipitated the financial crisis and led to the failure of Lehman Brothers, a major investment bank, numerous large commercial banks, such as Wachovia, and even the Federal National Mortgage Corporation (Fannie Mae), which had to be nationalized—that is, taken over by the federal government. One response to the financial crisis was the Dodd-Frank Act, which attempted major reforms of the financial system. The legislation’s purpose, as noted on dodd-frank.com is:

To promote the financial stability of the United States by improving accountability and transparency in the financial system, to end “too big to fail,” to protect the American taxpayer by ending bailouts, [and] to protect consumers from abusive financial services practices. . .

We will explore the financial crisis and the Great Recession in more detail in the macroeconomic chapters of this book, but for now it should be clear that many Americans have grown disenchanted with deregulation, at least of financial markets.

All market-based economies operate against a background of laws and regulations, including laws about enforcing contracts, collecting taxes, and protecting health and the environment. The government policies discussed in this chapter—like blocking certain anticompetitive mergers, ending restrictive practices, imposing price cap regulation on natural monopolies, and deregulation—demonstrate the role of government to strengthen the incentives that come with a greater degree of competition.

Intimidating Potential Competition

Businesses have developed a number of schemes for creating barriers to entry by deterring potential competitors from entering the market. One method is known as predatory pricing, in which a firm uses the threat of sharp price cuts to discourage competition. Predatory pricing is a violation of U.S. antitrust law, but it is difficult to prove.

Consider a large airline that provides most of the flights between two particular cities. A new, small start-up airline decides to offer service between these two cities. The large airline immediately slashes prices on this route to the bone, so that the new entrant cannot make any money. After the new entrant has gone out of business, the incumbent firm can raise prices again.

After this pattern is repeated once or twice, potential new entrants may decide that it is not wise to try to compete. Small airlines often accuse larger airlines of predatory pricing: in the early 2000s, for example, ValuJet accused Delta of predatory pricing, Frontier accused United, and Reno Air accused Northwest. In late 2009, the American Booksellers Association, which represents independently owned and often smaller bookstores, accused Amazon, Wal-Mart, and Target of predatory pricing for selling new hardcover best-sellers at low prices.

In some cases, large advertising budgets can also act as a way of discouraging the competition. If the only way to launch a successful new national cola drink is to spend more than the promotional budgets of Coca-Cola and Pepsi Cola, not too many companies will try. A firmly established brand name can be difficult to dislodge.

Summing Up Barriers to Entry

Table 3 lists the barriers to entry that have been discussed here. This list is not exhaustive, since firms have proved to be highly creative in inventing business practices that discourage competition. When barriers to entry exist, perfect competition is no longer a reasonable description of how an industry works. When barriers to entry are high enough, monopoly can result.

| Barrier to Entry | Government Role? | Example |

| Natural monopoly | Government often responds with regulation (or ownership) | Water and electric companies |

| Control of a physical resource | No | DeBeers for diamonds |

| Legal monopoly | Yes | Post office, past regulation of airlines and trucking |

| Patent, trademark, and copyright | Yes, through protection of intellectual property | New drugs or software |

| Intimidating potential competitors | Somewhat | Predatory pricing; well-known brand names |

How a Profit-Maximizing Monopoly Chooses Output and Price

Consider a monopoly firm, comfortably surrounded by barriers to entry so that it need not fear competition from other producers. How will this monopoly choose its profit-maximizing quantity of output, and what price will it charge? Profits for the monopolist, like any firm, will be equal to total revenues minus total costs. The pattern of costs for the monopoly can be analyzed within the same framework as the costs of a perfectly competitive firm—that is, by using total cost, fixed cost, variable cost, marginal cost, average cost, and average variable cost. However, because a monopoly faces no competition, its situation and its decision process will differ from that of a perfectly competitive firm.

Demand Curves Perceived by a Perfectly Competitive Firm and by a Monopoly

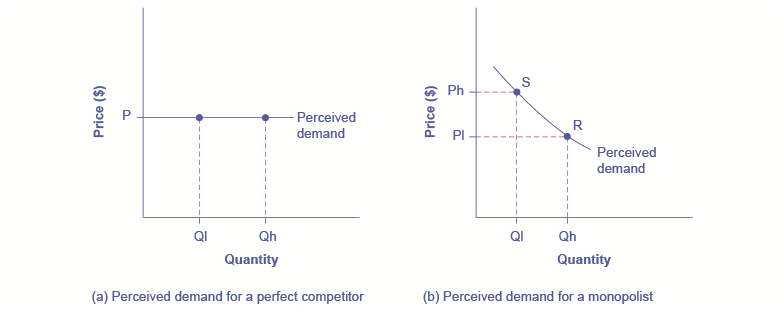

A perfectly competitive firm acts as a price taker, so its calculation of total revenue is made by taking the given market price and multiplying it by the quantity of output that the firm chooses. The demand curve as it is perceived by a perfectly competitive firm appears in Figure 6 (a). The flat perceived demand curve means that, from the viewpoint of the perfectly competitive firm, it could sell either a relatively low quantity like Ql or a relatively high quantity like Qh at the market price P.

The Perceived Demand Curve for a Perfect Competitor and a Monopolist

(a) A perfectly competitive firm perceives the demand curve that it faces to be flat. The flat shape means that the firm can sell either a low quantity (Ql) or a high quantity (Qh) at exactly the same price (P). (b) A monopolist perceives the demand curve that it faces to be the same as the market demand curve, which for most goods is downward-sloping. Thus, if the monopolist chooses a high level of output (Qh), it can charge only a relatively low price (Pl); conversely, if the monopolist chooses a low level of output (Ql), it can then charge a higher price (Ph). The challenge for the monopolist is to choose the combination of price and quantity that maximizes profits.

What is the Difference between Perceived Demand and Market Demand?

The demand curve as perceived by a perfectly competitive firm is not the overall market demand curve for that product. However, the firm’s demand curve as perceived by a monopoly is the same as the market demand curve. The reason for the difference is that each perfectly competitive firm perceives the demand for its products in a market that includes many other firms; in effect, the demand curve perceived by a perfectly competitive firm is a tiny slice of the entire market demand curve. In contrast, a monopoly perceives the demand for its product in a market where the monopoly is the only producer.

While a monopolist can charge any price for its product, that price is nonetheless constrained by demand for the firm’s product. No monopolist, even one that is thoroughly protected by high barriers to entry, can require consumers to purchase its product. Because the monopolist is the only firm in the market, its demand curve is the same as the market demand curve, which is, unlike that for a perfectly competitive firm, downward-sloping.

Figure 6 illustrates this situation. The monopolist can either choose a point like R with a low price (Pl) and high quantity (Qh), or a point like S with a high price (Ph) and a low quantity (Ql), or some intermediate point. Setting the price too high will result in a low quantity sold, and will not bring in much revenue. Conversely, setting the price too low may result in a high quantity sold, but because of the low price, it will not bring in much revenue either. The challenge for the monopolist is to strike a profit-maximizing balance between the price it charges and the quantity that it sells. But why isn’t the perfectly competitive firm’s demand curve also the market demand curve? See the following Clear it Up feature for the answer to this question.

What Defines the Market?

A monopoly is a firm that sells all or nearly all of the goods and services in a given market. But what defines the “market”?

In a famous 1947 case, the federal government accused the DuPont company of having a monopoly in the cellophane market, pointing out that DuPont produced 75% of the cellophane in the United States. DuPont countered that even though it had a 75% market share in cellophane, it had less than a 20% share of the “flexible packaging materials,” which includes all other moisture-proof papers, films, and foils. In 1956, after years of legal appeals, the U.S. Supreme Court held that the broader market definition was more appropriate, and the case against DuPont was dismissed.

Questions over how to define the market continue today. True, Microsoft in the 1990s had a dominant share of the software for computer operating systems, but in the total market for all computer software and services, including everything from games to scientific programs, the Microsoft share was only about 16% in 2000. The Greyhound bus company may have a near-monopoly on the market for intercity bus transportation, but it is only a small share of the market for intercity transportation if that market includes private cars, airplanes, and railroad service. DeBeers has a monopoly in diamonds, but it is a much smaller share of the total market for precious gemstones and an even smaller share of the total market for jewelry. A small town in the country may have only one gas station: is this gas station a “monopoly,” or does it compete with gas stations that might be five, 10, or 50 miles away?

In general, if a firm produces a product without close substitutes, then the firm can be considered a monopoly producer in a single market. But if buyers have a range of similar—even if not identical—options available from other firms, then the firm is not a monopoly. Still, arguments over whether substitutes are close or not close can be controversial.

The Inefficiency of Monopoly

Most people criticize monopolies because they charge too high a price, but what economists object to is that monopolies do not supply enough output to be allocatively efficient. To understand why a monopoly is inefficient, it is useful to compare it with the benchmark model of perfect competition.

Allocative efficiency is a social concept. It refers to producing the optimal quantity of some output, the quantity where the marginal benefit to society of one more unit just equals the marginal cost. The rule of profit maximization in a world of perfect competition was for each firm to produce the quantity of output where P = MC, where the price (P) is a measure of how much buyers value the good and the marginal cost (MC) is a measure of what marginal units cost society to produce. Following this rule assures allocative efficiency. If P > MC, then the marginal benefit to society (as measured by P) is greater than the marginal cost to society of producing additional units, and a greater quantity should be produced. But in the case of monopoly, price is always greater than marginal cost at the profit-maximizing level of output, as can be seen by looking back at Figure 6. Thus, consumers will suffer from a monopoly because a lower quantity will be sold in the market, at a higher price, than would have been the case in a perfectly competitive market.

The problem of inefficiency for monopolies often runs even deeper than these issues, and it also involves incentives for efficiency over longer periods of time. There are counterbalancing incentives here. On one side, firms may strive for new inventions and new intellectual property because they want to become monopolies and earn high profits—at least for a few years until the competition catches up. In this way, monopolies may come to exist because of competitive pressures on firms. However, once a barrier to entry is in place, a monopoly that does not need to fear competition can just produce the same old products in the same old way—while still ringing up a healthy rate of profit. John Hicks, who won the Nobel Prize for economics in 1972, wrote in 1935, “The best of all monopoly profits is a quiet life.” He did not mean the comment in a complimentary way. He meant that monopolies may bank their profits and slack off on trying to please their customers.

When AT&T provided all of the local and long-distance phone service in the United States, along with manufacturing most of the phone equipment, the payment plans and types of phones did not change much. The old joke was that you could have any color phone you wanted, as long as it was black. In 1982, AT&T was split by government litigation into a number of local phone companies, a long-distance phone company, and a phone equipment manufacturer. An explosion of innovation followed. Services like call waiting, caller ID, three-way calling, voice mail though the phone company, mobile phones, and wireless connections to the Internet all became available. A wide-range of payment plans was also offered. It was no longer true that all phones were black; instead, phones came in a variety of shapes and colors. The end of the telephone monopoly brought lower prices, a greater quantity of services, and also a wave of innovation aimed at attracting and pleasing customers.

A monopolist is not a price taker, because when it decides what quantity to produce, it also determines the market price. For a monopolist, total revenue is relatively low at low quantities of output, because not much is being sold. Total revenue is also relatively low at very high quantities of output, because a very high quantity will sell only at a low price. Thus, total revenue for a monopolist will start low, rise, and then decline. The marginal revenue for a monopolist from selling additional units will decline. Each additional unit sold by a monopolist will push down the overall market price, and as more units are sold, this lower price applies to more and more units.

The monopolist will select the profit-maximizing level of output where MR = MC, and then charge the price for that quantity of output as determined by the market demand curve. If that price is above average cost, the monopolist earns positive profits.

Monopolists are not productively efficient, because they do not produce at the minimum of the average cost curve. Monopolists are not allocatively efficient, because they do not produce at the quantity where P = MC. As a result, monopolists produce less, at a higher average cost, and charge a higher price than would a combination of firms in a perfectly competitive industry. Monopolists also may lack incentives for innovation, because they need not fear entry.

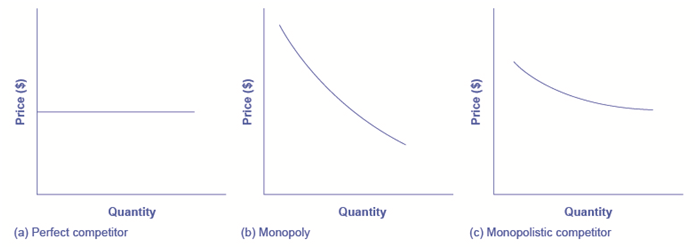

Monopolistic Competition and Oligopoly

Perfect competition and monopoly are at opposite ends of the competition spectrum. A perfectly competitive market has many firms selling identical products who all act as price takers in the face of the competition. If you recall, price takers are firms that have no market power. They simply have to take the market price as given.

Monopoly arises when a single firm sells a product for which there are no close substitutes. Microsoft, for instance, has been considered a monopoly because of its domination of the operating systems market.

What about the vast majority of real world firms and organizations that fall between these extremes, firms that could be described as imperfectly competitive? What determines their behavior? They have more influence over the price they charge than perfectly competitive firms, but not as much as a monopoly would. What will they do?

One type of imperfectly competitive market is called monopolistic competition. Monopolistically competitive markets feature a large number of competing firms, but the products that they sell are not identical. Consider, as an example, the Mall of America in Minnesota, the largest shopping mall in the United States. In 2010, the Mall of America had 24 stores that sold women’s “ready-to-wear” clothing (like Ann Taylor and Coldwater Creek), another 50 stores that sold clothing for both men and women (like Banana Republic, J. Crew, and Nordstrom’s), plus 14 more stores that sold women’s specialty clothing (like Motherhood Maternity and Victoria’s Secret). Most of the markets that consumers encounter at the retail level are monopolistically competitive.